How Inflation Affects Your Financial Plan

April 25, 2022

Content updated as of May 12, 2022

Concerned about how inflation affects your finances? Look to historical data to quell fears and stay the course of your financial plan.

As April drew to a close, there was no question America was facing rapidly increasing inflation. It reached its highest pace since 1982: 8.3% for April 2022. Because of this recent rise in inflation, it is one of the most common concerns on our clients’ minds, both in how we are thinking about investments and how this will affect their financial plans. It’s worth exploring some historical perspectives to apply what we’ve learned from past cycles to move confidently through what’s ahead.

Put simply, inflation is the general increase in prices and fall in purchasing power. To illustrate, the average retail price of a pound of bacon in 1970 was $0.82 per pound; in 2021 it was $7.21 per pound. That’s an 879% increase! In the United States, the most commonly used measure of inflation is the Consumer Price Index (CPI). The CPI is compiled by the U.S. Bureau of Labor and Statistics and represents the changes in prices of all goods and services purchased for consumption by urban households.

Historical Perspective, Federal Reserve and Expectations

Since 1914, inflation has averaged 3.2%. Over the last 30 years, inflation has averaged 2.3%. The Federal Reserve, which is the central bank of the United States, conducts the nation’s monetary policy with a goal to promote maximum employment, stable prices, and moderate long term interest rates. In 2012, it introduced a long-term goal of 2% inflation. Then in 2020, it introduced a concept called average inflation targeting, meaning inflation would be allowed to run above 2% after periods of lower than 2% inflation. Since 2009, average inflation is 1.8%, and the Fed has exercised that average inflation targeting by letting inflation run above that 2% target.

The last two years have undoubtedly added pressure to what we’re seeing. Due to supply chain issues related to the Covid-19 pandemic, a return in demand with Covid-19 lockdowns ending, and now a war between Russia and Ukraine, inflation has gotten a bit ahead of the Fed, averaging 4.7% in 2021 and on track to be above 7% for 2022. This won’t magically disappear tomorrow. United States Secretary of the Treasury, Janet Yellen, recently stated we should expect another 12 months of “uncomfortably high inflation.” The ICE Benchmark Administration is pricing inflation expectations at an average of 2.9% between 2023 and 2028, followed by 2.6% in the years heading into 2032.

Impact of Inflation on Financial Markets

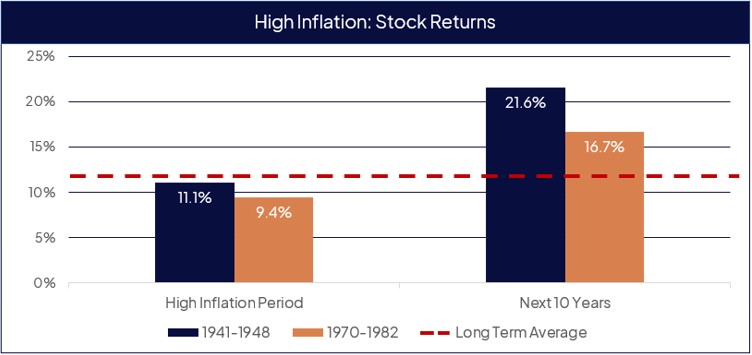

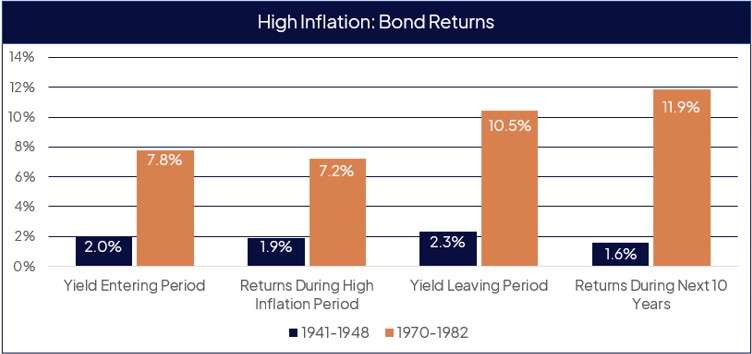

Let’s take a look at prior periods of high inflation to see how they impacted investment returns. Two historic periods of high inflation were 1941-1948 (avg. inflation was 7.1%) and 1970-1982 (avg. inflation was 7.75%).

Stock returns (measured by the S&P 500 Index) during those time periods were roughly in line with historical averages, and the 10 years following the high inflation period returns were greater than average.

Bond returns (measured by 10-year treasury) were roughly in line with yield going into those time periods and following 10-year returns were mixed but again, relatively close to yields entering that period. One difference is that interest rates didn’t increase as much during the 1941-1948 timespan.

Inflation and Your Financial Planning

When putting together a financial plan for our clients, we typically use 2.5% as our long-term inflation target (0.5% higher than the Fed’s long-term goal). This considers that inflation is currently higher and assumes that it will revert to the average and Fed target over time. For clients with shorter time horizons, or clients that are particularly worried about inflation, we have tools at our disposal to determine how higher inflation numbers could impact their plan. First, we can use stress tests to illustrate how higher levels of inflation over the length of your plan would impact your outcomes. Second, we can increase current spending assumptions to simulate a shorter period of higher inflation, followed by normal inflation.

For you, this means take a deep breath and remember: This too shall pass. It’s always a good idea to periodically review your financial plan with your advisor for peace of mind. If you are considering making changes to your portfolio, work closely with your advisor to understand how those changes will affect the long-term outcomes in your financial plan. It is hard to predict when these trends will reverse, but mean reversion is a pervasive force. This concept states that in a time series (like inflation from year to year) outcomes tend to revert to their long-term average.

Consider, however, if we do observe extended, higher levels of inflation, those periods have historically been followed by strong returns in equity markets. These higher-than-average returns can help offset some of the increased costs brought on by inflation, as they would exceed the conservative return assumptions we use in planning.

By drawing confidence from a sound financial plan, one that positions you well in the market, you’ll be ready for the unexpected. Swings in inflation rates are no exception. If you’d like to learn more about how a financial plan can help prepare you for the unexpected, like rising inflation rates, contact us to meet with a Freestone client advisor.

Important Disclosures: Nothing in this article is intended to provide, and you should not rely upon it for, accounting, legal, tax or investment advice or recommendations. We are not making any specific recommendations regarding your financial plan or any investment strategies, and you should not make any decisions regarding such strategies based on the information in this document. The intention of this document is educational, and it is intended only to discuss limited aspects of inflation and how it could potentially affect your current financial situation. This article is not a comprehensive or complete summary of considerations regarding inflation. Each individual is in a different situation and has different items to address, and the options in this document are not appropriate for everyone.

This article speaks only as of the date indicated. While we believe the information in this article is reliable, we do not make any representation or warranty concerning the accuracy of any data in this article and we disclaim any liability arising out of your use of, or reliance on, such information. The information and opinions in this article are subject to change without notice, and we do not undertake any responsibility to update any information in this article or advise you of any change in such information in the future.

Portions of this article constitute “forward-looking statements” and are subject to a number of significant risks and uncertainties. Any such forward-looking statements should not be relied upon as predictions of future events or results. Past performance of any investment or wealth management strategy or program is not a reliable indicator of future results. Please consult your Freestone client advisor regarding options specific to your needs.