Investment Truths in an Uncertain World

May 25, 2022

There is always a feeling of unease when the markets become volatile. Volatility can be created by any market event or crisis, whether it is news of inflation, geopolitical events, or government interventions. As humans, we often feel the need to take action or to do something when faced with uncertainty. These reactive responses are often driven by emotion such as fear or greed and can often be the wrong motivators. We counsel our clients to pause and reflect on these valuable investment truths during uncertain times.

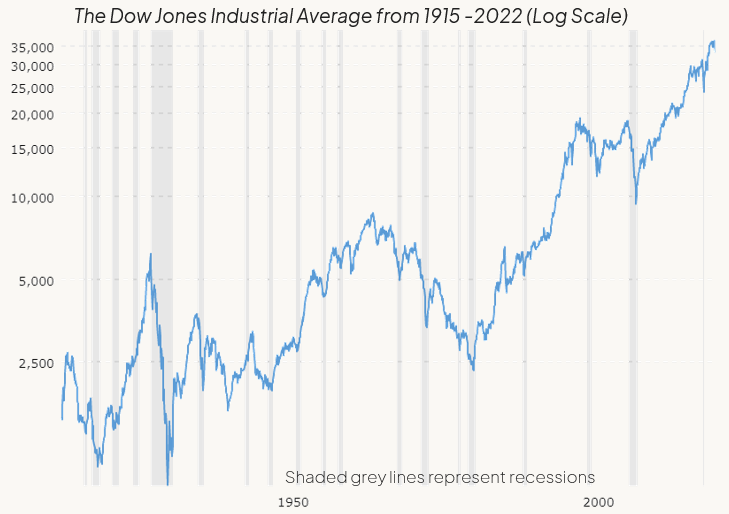

#1 We’ve recovered from every recession and depression

The markets are surprisingly resilient. To date, we’ve recovered from every downturn, and the economy has continued to grow over time. Both the pandemic and global sanctions on various industries have shed light on the fragility of some industries, and the strength of others. Historically, a globally diversified portfolio has been able to offset company-specific risk and allowed it to grow over time.

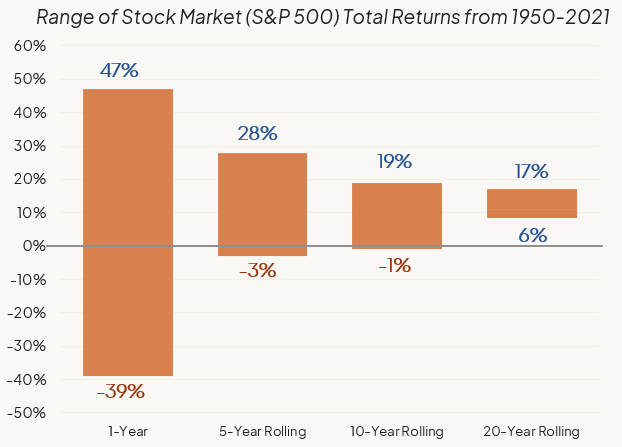

#2 Time is on our side

For those who invested in the U.S. stock market on any given day since the mid-1950s, and stayed invested for 15-20 years, their chances of a positive return was over 99%. While there have been lost decades of low return and high volatility (think March 2000 through June 2013), thinking long-term has allowed investors to participate in portfolio growth over time. With a longer investment horizon, we feel confident investing in equities for long-term returns.

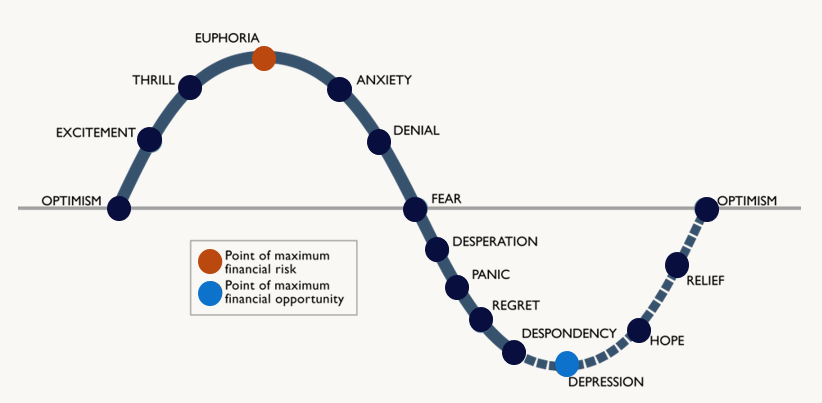

#3 Stick to the plan

The times in which hope feels lost are often when financial returns can be made. These thoughts really resonate in those pivotal moments:

- “Be fearful when others are greedy, and greedy when others are fearful.” – Warren Buffet

- – Howard Marks, Oaktree Capital (March 2022 memo)

Many clients feel the need to do something during these emotional low points. Doing nothing is also a choice. Rebalancing can be hard, but rewarding. Dollar Cost Averaging plans often help clients stay in that happy medium. This is when your careful planning does the work; there’s no earned interest on worrying.

#4 Don’t wait for the perfect time

If you’ve been actively saving over many years, you might be inclined to sit on the sidelines amassing cash, waiting for the best time to buy into the market. In reviewing equity returns over the past 20 years, we find that the greatest danger is to stay in cash. In fact, staying in cash has provided significantly smaller returns than someone who has picked the “worst time to buy,” such as when the market reaches its highest point every single year.

#5 Don’t two-time the market (and regret missing gains)

Seven out of the top ten best days in the past 20 years happened after some of the worst days over the same period. One gut reaction might be to sell out of the market to avoid the worst days, but then you’d have to be right twice by selling and then buying back in to be able to outperform. According to JP Morgan’s Principles for Successful Investing data in 2020, by staying fully invested in equities over the past 20 years, you would have annualized 7.5% over that span. By missing just 20 of the best days within these past 20 years (consider that’s only 20 out of 5,030 trading days!) your investment return would essentially have been flat. The average investor has annualized just 2.9% return over the past 20 years, showing that the average investor is not good at timing the market.

#6 Ignore the noise

Media has different goals than you. There’s no question news can influence consumer behavior. Sometimes coverage of the Fed can steer markets in a direction with just a whiff of suggestion about an interest rate change. These sound bites can drive emotional and hasty decisions. Plan on riding out volatile markets because they happen often. Intra-year declines in the S&P 500 have averaged -13.7% since the 1950s, yet the annual returns have been positive in 51 of those 70 calendar years. It is okay to start investing slowly, but the larger goals should be to get fully invested. Try dollar-cost-averaging to smooth your ride into and out of the markets and know your goals. Allow yourself the comfort to invest in growth assets for long-term goals.

When you invest, there is always some sort of risk associated. And becoming comfortable with the volatility is part of the equation. Understanding the data can help quell fears or anxieties and allow you to make clear and unemotional decisions about your investments. At Freestone, we work closely with our clients to understand their risk tolerance and allocate their investments accordingly. If you’d like to learn more about Freestone and our philosophy behind investing, please contact us to learn more.

Important Disclosures: This article contains general information, opinions and market commentary and is only a summary of certain issues and events that we believe may be of interest generally. Nothing in this article is intended to provide, and you should not rely on it for, accounting, legal, tax or investment advice or recommendations. We are not making any specific recommendations regarding any security, asset class or investment or wealth management strategy, and you should not make any decisions based on the information in this article. Instead, you should consult your Freestone client advisor regarding options specific to your circumstances before taking any action. While we believe the information in this article is reliable, we do not make any representation or warranty concerning the accuracy of any third-party data in this article and we disclaim any liability arising out of your use of, or reliance on, such information. The information and opinions in this article are subject to change without notice, and we do not undertake any responsibility to update any information herein or advise you of any change in such information in the future. This article speaks only as of the date indicated. Past performance of any investment or wealth management strategy or program is not a reliable indicator of future results. Portions of this article constitute “forward-looking statements” and are subject to a number of significant risks and uncertainties. Any such forward-looking statements should not be relied upon as predictions of future events or results.