Navigating Uncertainty: Oil Shocks, Volatility, and the Case for Staying Invested

April 16, 2026

The first quarter of 2026 was defined by a single, jarring event: the outbreak of conflict between the United States and Iran. Oil prices surged. Inflation risks re-emerged just as they were fading. Equity markets sold off.

Uncertainty and volatility are a normal part of market behavior. History and data offer important perspective on what happened, and why the case for staying invested remains intact.

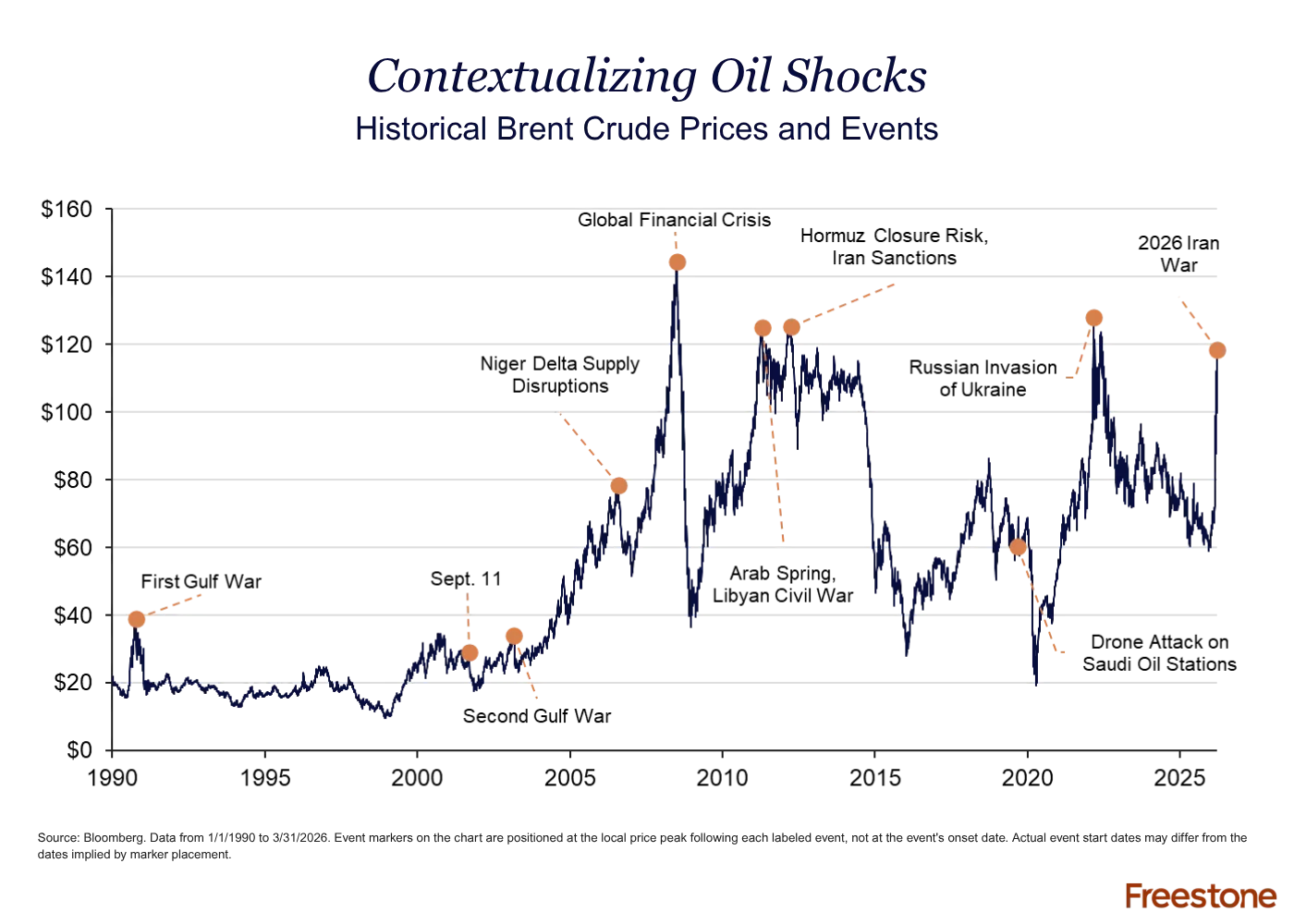

What Happened to Oil Prices During the US-Iran Conflict?

The Iran conflict triggered one of the sharpest spikes in oil prices in modern history, driven by disruption to global trade that flows through the Strait of Hormuz.

- Roughly 20% of the world’s oil supply transits the Strait of Hormuz. Oil disruptions feed higher energy costs through increased costs to consumers and businesses.

- Why this matters: Context matters more than headlines. Historically, oil supply disruptions have been painful in the short term but have consistently eventually moderated as supply adjustments and diplomatic efforts took hold. Investors who responded with patience rather than panic have historically been better positioned as conditions normalized.

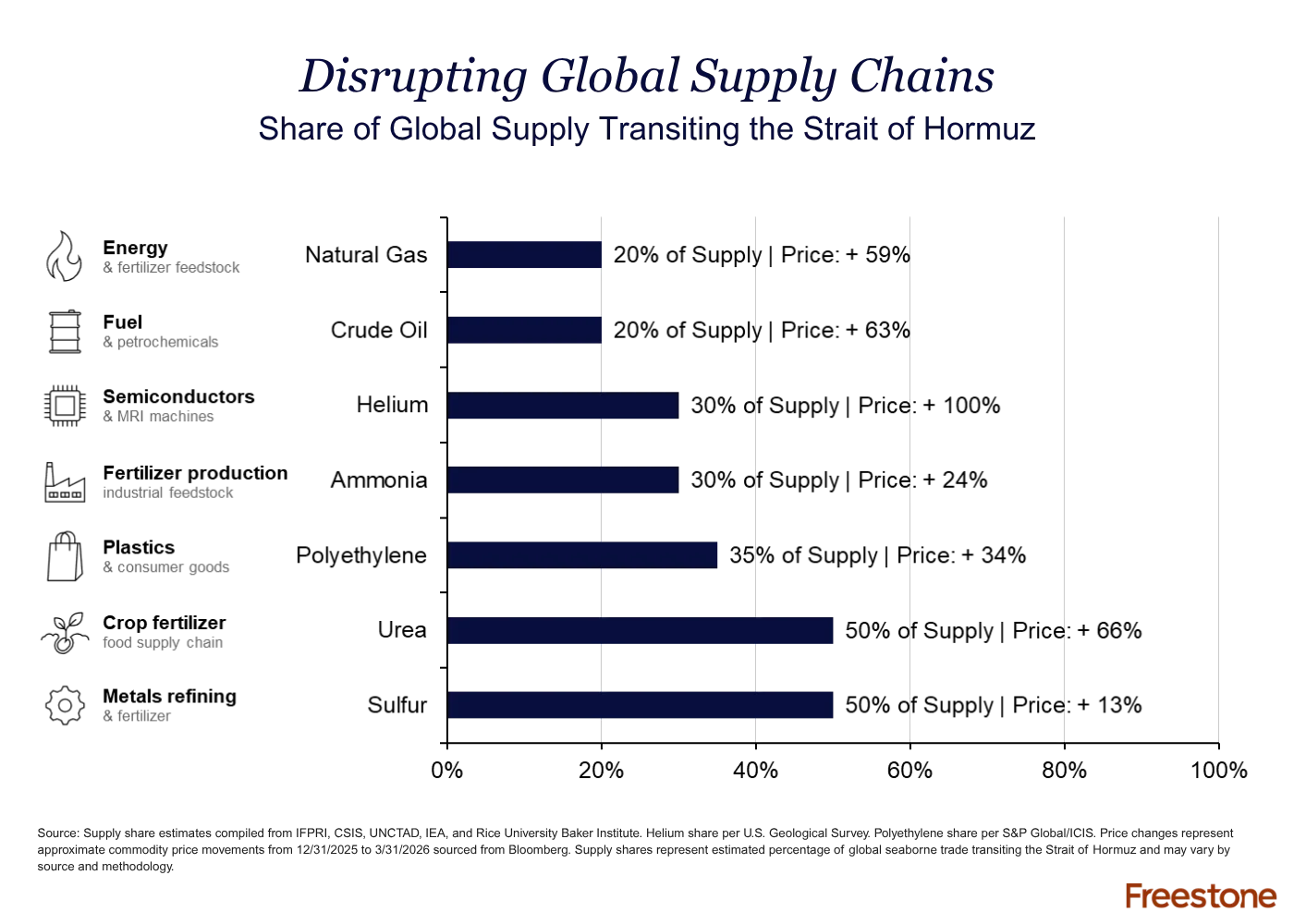

How Does a Strait of Hormuz Disruption Impact the Broader Economy?

The Strait of Hormuz carries far more than crude oil, and commodity price increases illustrate the importance of the Strait to global trade.

- The Strait is a critical transit route for fertilizer, petrochemicals, helium, and other commodities that feed into food production, semiconductor manufacturing, medical equipment, and consumer goods. Price increases can show up in grocery bills, healthcare costs, and consumer goods within months.

- Why this matters: Commodity price increases could spur inflation and limit global growth. Sustained commodity inflation could keep inflation above the Fed’s 2% target longer, reducing flexibility for rate cuts — the key risk we are watching heading into the second half of the year.

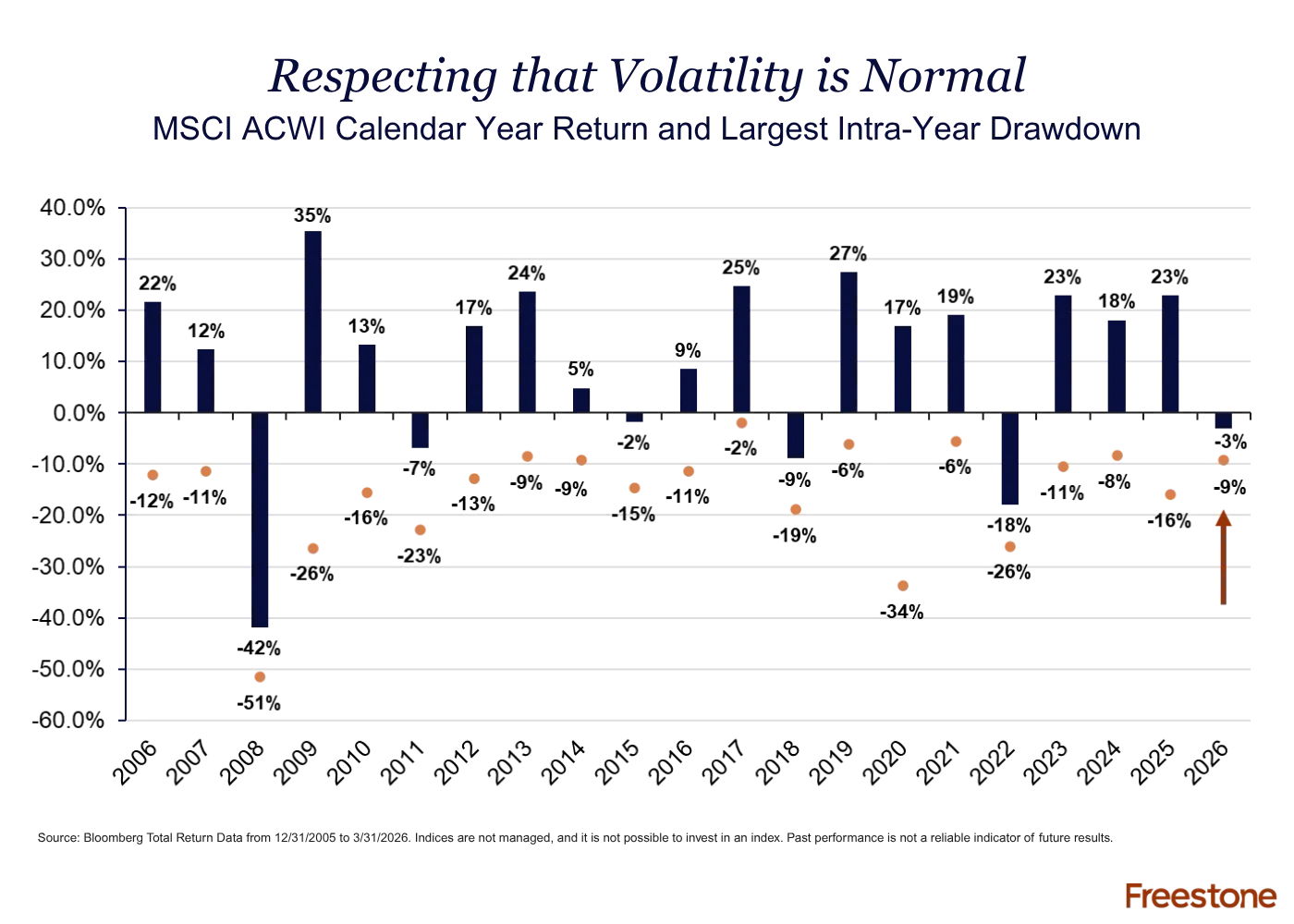

How Normal is Market Volatility?

Q1 also served as a broader reminder that drawdowns are a normal and recurring part of investing, not a signal that the market is broken. Almost every calendar year includes a meaningful pullback, yet in most of those years, markets finished with positive returns.

- Since 2005, global equities (MSCI ACWI) have averaged approximately 11% annual returns despite an average intra-year drawdown of approximately 16%. Volatility and strong long-term returns have coexisted, not competed.

- Why this matters: Drawdowns are the price of admission for long-term equity returns. Investors who have captured those returns are the ones who stayed invested through the uncomfortable moments.

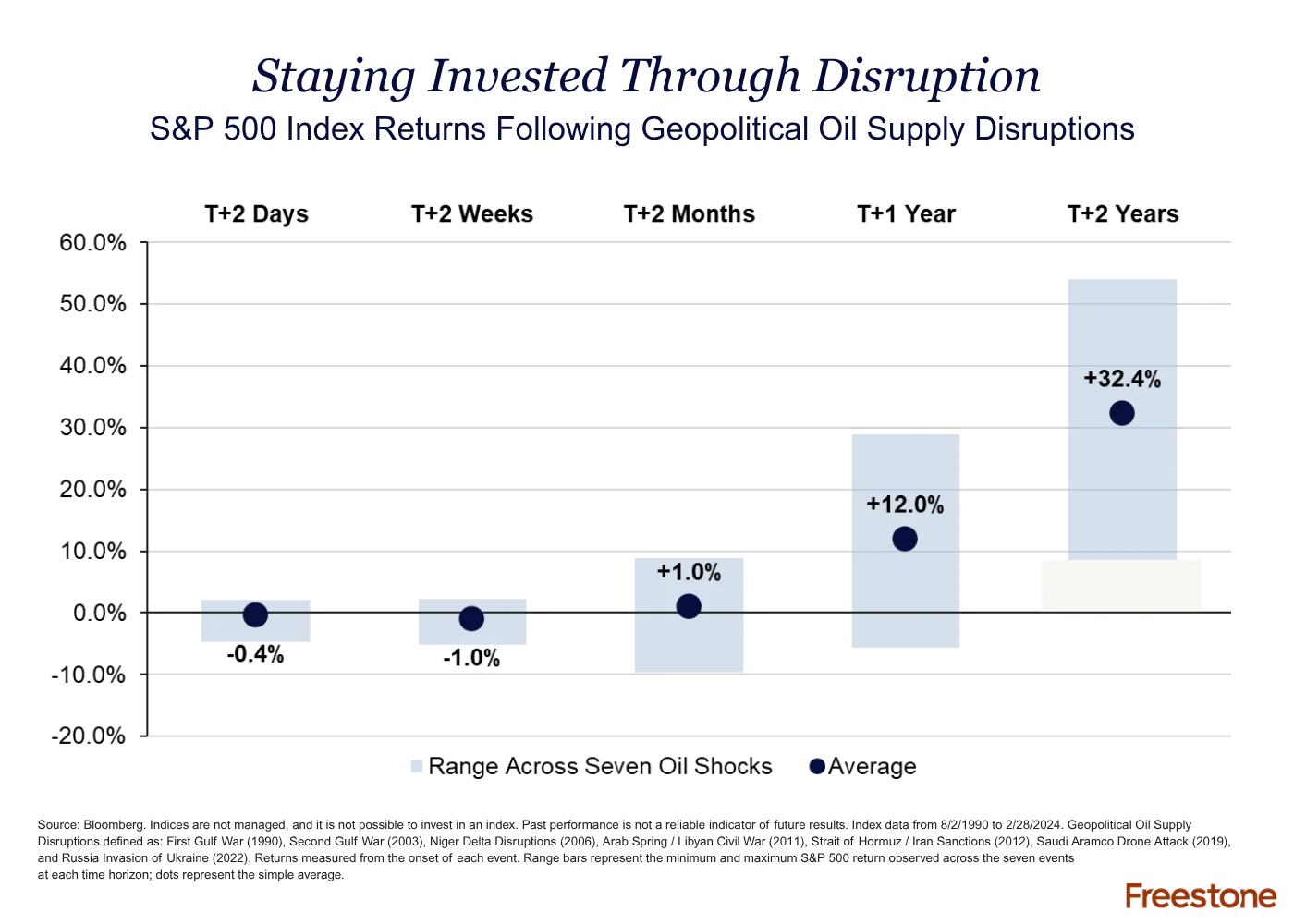

How Have Markets Rebounded from Disruptions Like This Before?

Geopolitical oil supply disruptions tend to trigger immediate selloffs as investors process uncertainty. But the historical record shows that staying invested has consistently been the right call.

- Across seven major geopolitical oil supply disruptions since 1990, the S&P 500 typically declined in the first month due to uncertainty, while rising 12.0% on average after one year.

- Why this matters: Geopolitical oil supply shocks have led to near-term equity market weakness, but stronger forward returns, reinforcing the importance of staying invested through periods of conflict-driven volatility.

The Case for Staying Invested

Q1 2026 was volatile, but the data supports the narrative that oil and supply shocks have occurred throughout market history, and investors who responded with discipline rather than fear have consistently benefited from staying invested.

Broad equity fundamentals remain solid, and diversification continues to position portfolios to navigate a range of potential outcomes. While near-term volatility may persist, maintaining exposure has historically been a more reliable path to long-term outcomes than reacting to short-term uncertainty.

Disclosures: For educational and discussion purposes only. Nothing herein is intended to provide, and it should not be relied upon for, accounting, legal, tax or investment advice or recommendations. We are not making any specific recommendations regarding any security or investment strategy, and you should not make any investing decisions based on the information herein. This document contains general information, opinions and market commentary and is only a summary of certain issues and events that we believe might be of interest generally. Opinions are subject to change without notice. While the information presented is believed to be reliable, no representation or warranty is made concerning the accuracy of any information provided, and we do not undertake any responsibility to update such information or advise you of any change in such information in the future. This document speaks only as of the date indicated. Indices referenced in this document are not managed and it is not possible to invest in an index. Past performance of any investment strategy is not a reliable indicator of future results. Links to third-party articles and/or websites are for general information purposes only, and not endorsed by us and you are encouraged to read and evaluate the privacy and security policies on the specific site you are entering.