Navigating Volatility: Understanding Tariff Impacts, Embracing Global Diversification, and Reassessing Valuations in Q2 2025

July 17, 2025

The second quarter of 2025 featured a dramatic shift in investor sentiment. Initially, markets were shaken by President Trump’s “Liberation Day” tariff announcement on foreign trade partners, but subsequent delays in implementing the tariffs and a limited number of trade deals ultimately brought relief to investors. Despite persistent tariff uncertainties, and geopolitical tensions intensified by the Iran-Israel conflict, robust corporate fundamentals propelled global equities through these challenges to reach new all-time highs. While the strong rebound in U.S. stocks has led to historically elevated valuations, bonds continue to offer investors appealing diversification benefits, with their high starting yields providing an attractive alternative to richly valued equity markets. Below, we explore the significance of these developments for investors and how we are positioning portfolios for what may lie ahead.

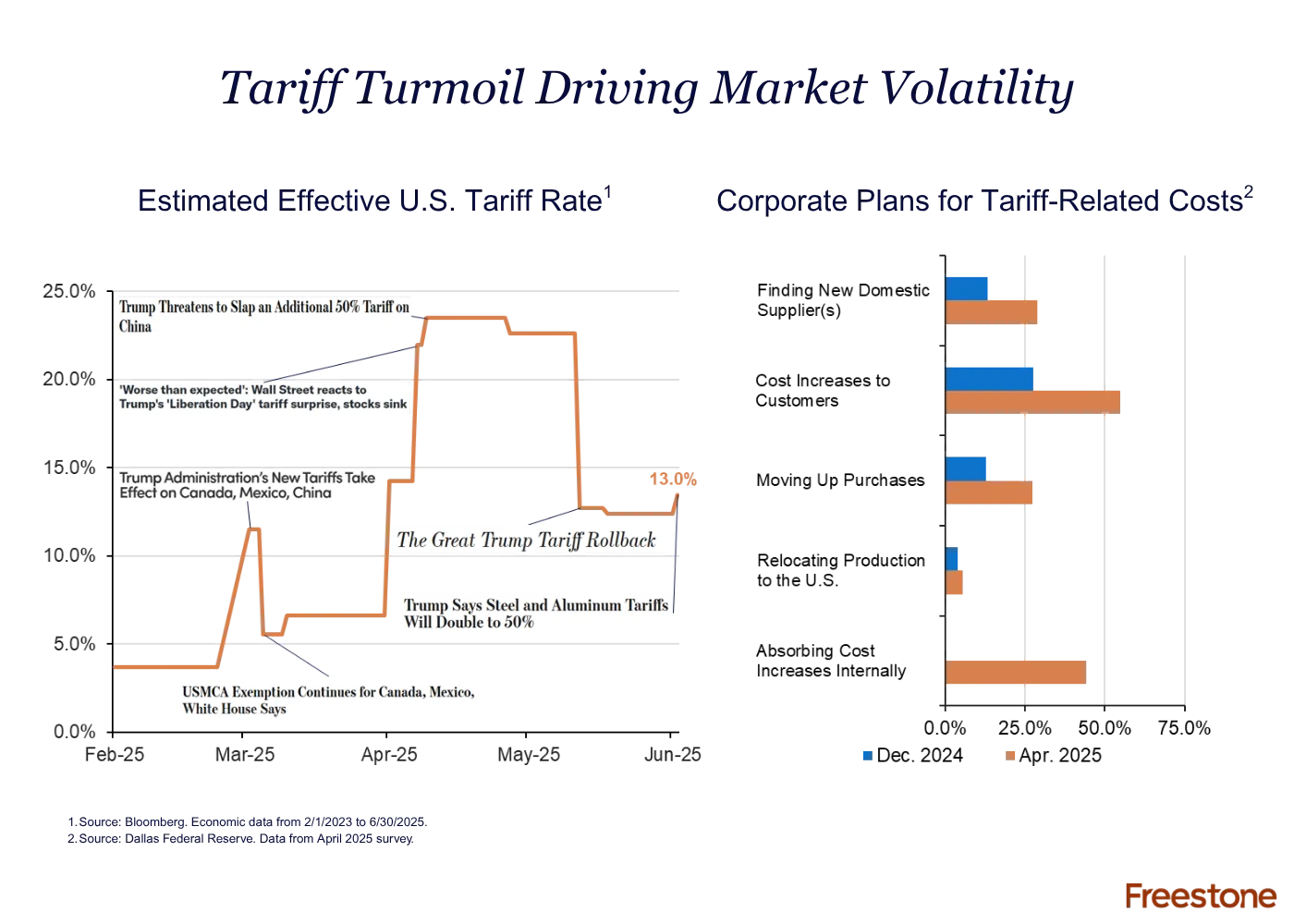

Tariff Turmoil Driving Market Volatility

Even though the U.S. has yet to collect on new tariff revenues from many foreign trade partners, that doesn’t mean tariffs haven’t already been felt by investors and corporations.

- Effective tariff rates spiked dramatically from under 5% at the year’s start to 23% after announcing a 50% tariff on China, before retreating to the low-teens. Whipsawing expectations for tariff policy deteriorated consumer sentiment and sparked significant market turbulence during the quarter, highlighted by the sharp sell-off following the Liberation Day announcement.

- While relatively few businesses are relocating production to the U.S. (increasing modestly from 3.9% to 5.5%), a larger proportion have indicated plans to either absorb increased costs internally (44.3%) or pass them on to consumers (54.7%), potentially impacting profitability and inflation.

- Tracking tariff developments is important for investors because prolonged uncertainty restricts business investments and negatively impacts growth while more restrictive tariffs can potentially fuel inflation.

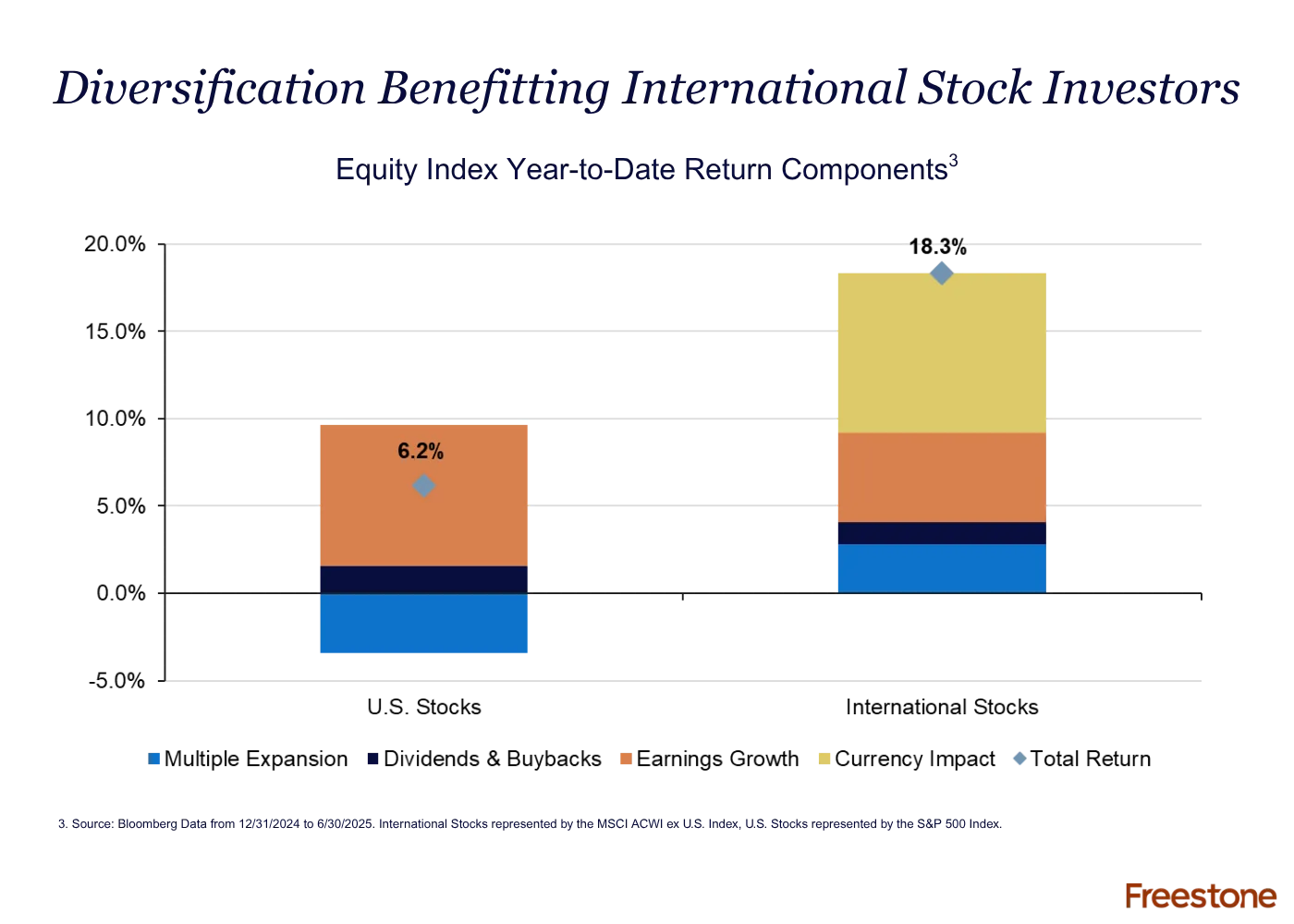

Diversification Benefitting International Stock Investors

Year-to-date returns for U.S. and international stocks diverged significantly despite both benefiting from positive earnings growth.

- U.S. stocks delivered a 6.2% return driven primarily by earnings growth but negatively impacted by valuation contraction. Conversely, international stocks outperformed by gaining 18.3%, boosted by a combination of earnings growth, valuation expansion, and notably, positive foreign currency returns against a falling U.S. dollar.

- U.S. investors in foreign stocks uniquely benefit from a falling dollar because it enhances the value of returns denominated in foreign currencies.

- As evidenced during the quarter, investors can benefit from geographic diversification without compromising on earnings growth or total returns, this consideration is especially crucial given elevated equity valuations and policy uncertainty in the U.S.

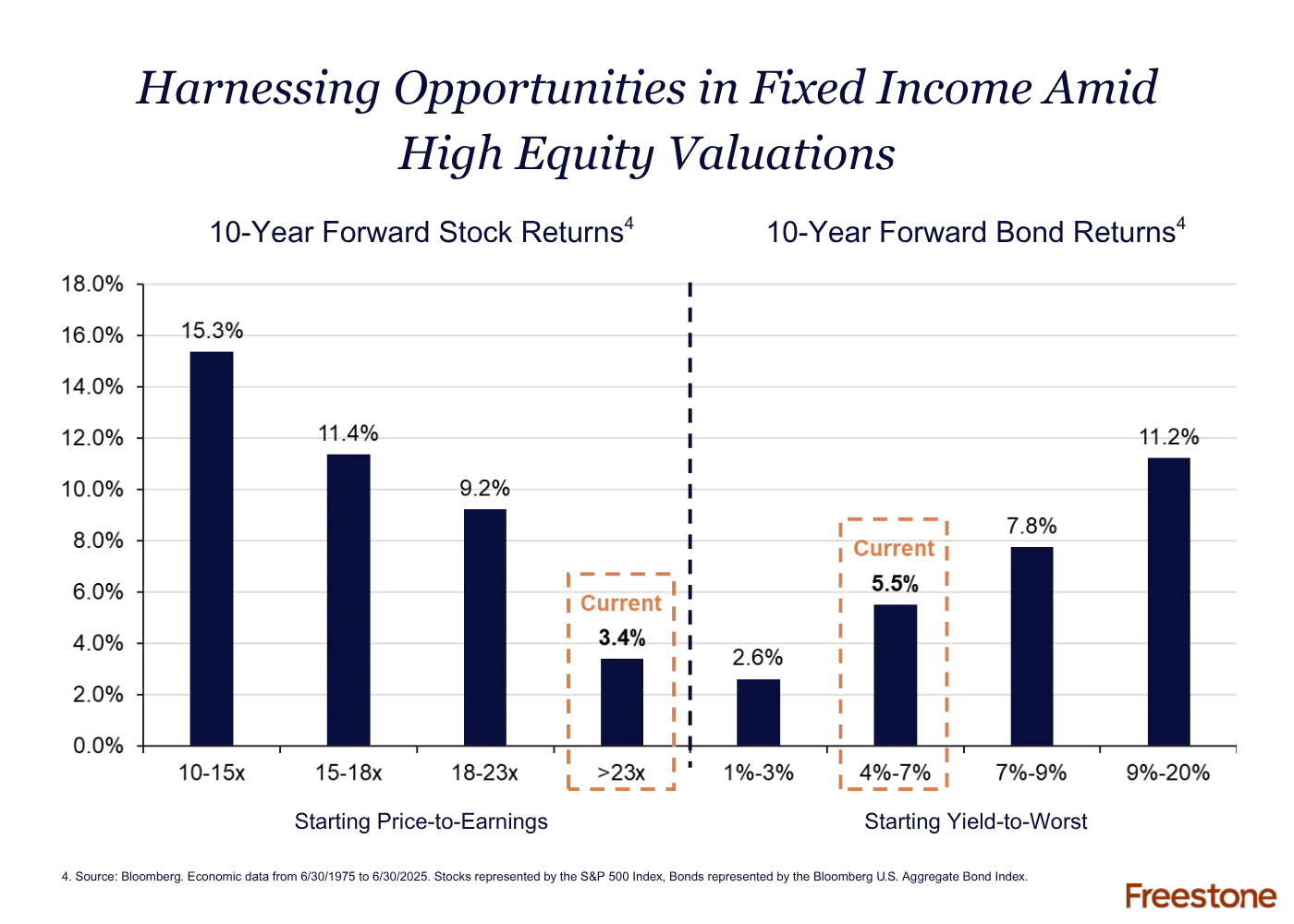

Harnessing Opportunities in Fixed Income Amid High Equity Valuations

Current fixed income valuations present compelling opportunities, particularly when compared with the lofty valuations currently observed in U.S. equity markets. Analyzing historical patterns of returns for stocks and bonds at various valuation levels underscores the attractiveness of today’s fixed income environment.

- When the S&P 500’s price-to-earnings ratio exceeds 23.0x (currently at 23.2x), average forward 10-year returns have historically been low, around 3.4% annually.

- Conversely, the Bloomberg U.S. Aggregate Bond Index, with its current yield-to-worst of 4.7%, historically offers attractive forward returns averaging about 5.5%.

- Considering these historical returns, investors may benefit from a diversified portfolio that includes both stocks and bonds. Improved expected returns for bonds not only help achieve portfolio return objectives but also can enhance downside protection so portfolios are positioned to proactively capitalize on opportunities during periods of volatility in equity markets.

Positioning Portfolios for Continued Uncertainty

Investors should recognize that this year’s market volatility was driven primarily by uncertainty rather than weakening economic fundamentals. While investor sentiment is fragile, the economic backdrop remains intact. However, with elevated equity valuations and persistent policy and geopolitical uncertainty likely to endure throughout 2025, we are prepared to navigate continued volatility. Emphasizing diversification geographically and across asset classes positions portfolios not only for stability but also to capitalize opportunistically during market stress.

1Source: Bloomberg. Economic data from 2/1/2023 to 6/30/2025.

2Source: Dallas Federal Reserve. Data from April 2025 survey.

3Source: Bloomberg Data from 12/31/2024 to 6/30/2025. International Stocks represented by the MSCI ACWI ex U.S. Index, U.S. Stocks represented by the S&P 500 Index

4Source: Bloomberg. Economic data from 6/30/1975 to 6/30/2025. Stocks represented by the S&P 500 Index, Bonds represented by the Bloomberg U.S. Aggregate Bond Index.

Disclosures: For educational and discussion purposes only. Nothing herein is intended to provide, and it should not be relied upon for, accounting, legal, tax or investment advice or recommendations. We are not making any specific recommendations regarding any security or investment strategy, and you should not make any investing decisions based on the information herein. This document contains general information, opinions and market commentary and is only a summary of certain issues and events that we believe might be of interest generally. Opinions are subject to change without notice. While the information presented is believed to be reliable, no representation or warranty is made concerning the accuracy of any information provided, and we do not undertake any responsibility to update such information or advise you of any change in such information in the future. This document speaks only as of the date indicated. Indices referenced in this document are not managed and it is not possible to invest in an index. Past performance of any investment strategy is not a reliable indicator of future results. Links to third-party articles and/or websites are for general information purposes only, and not endorsed by us and you are encouraged to read and evaluate the privacy and security policies on the specific site you are entering.