Washington State Millionaires Tax: What High-Income Families Should Know

March 17, 2026

All information below reflects legislative developments as of March 13, 2026. Because this is a rapidly evolving landscape, changes occurring after this date may not be reflected.

Washington State has advanced legislation that would impose a 9.9% income tax on annual earnings above $1 million. The measure recently passed the Washington State House and Senate and is now on its way to Governor Bob Ferguson, who has indicated he intends to sign the bill into law.

If enacted, the tax would apply beginning in 2028.

For high-income households, this proposal does not stand alone. It comes on the heels of two significant tax law changes Washington recently implemented — updates to the state’s long-term capital gains tax and its estate tax framework. Understanding how these layers work together is increasingly important for long-term planning.

What Is the Washington Millionaires Tax? (Quick Answer)

The proposed Washington Millionaires Tax would apply a 9.9% state tax to income above $1 million starting in tax year 2028. It applies only to earnings exceeding the threshold and would affect an estimated 20,000–30,000 households.

How Would the 9.9% Tax Work?

The legislation would:

- Impose a 9.9% tax on household income above $1 million

- Apply only to the amount exceeding $1 million

- Example: A taxpayer with $1.5 million of income would owe tax on $500,000

- Taxpayers will receive a $1 million exemption per household regardless of tax filing status (e.g. married filing jointly or single)

- Take effect in tax year 2028 (returns filed in 2029)

- Generate an estimated $4 billion annually

The $1 million threshold is applied to the household adjusted gross income (AGI) reported on their federal tax return.

AGI includes wages, business income, capital gains, bonus compensation, rental income, and other taxable income. As a result, even households with consistent annual income below $1 million could exceed the threshold in a year with significant liquidity events such as a business sale, large capital gains, or other one-time income events.

How the Millionaires Tax Fits Into Washington’s Broader Tax Changes

The proposed income tax follows two major tax law changes already implemented in Washington.

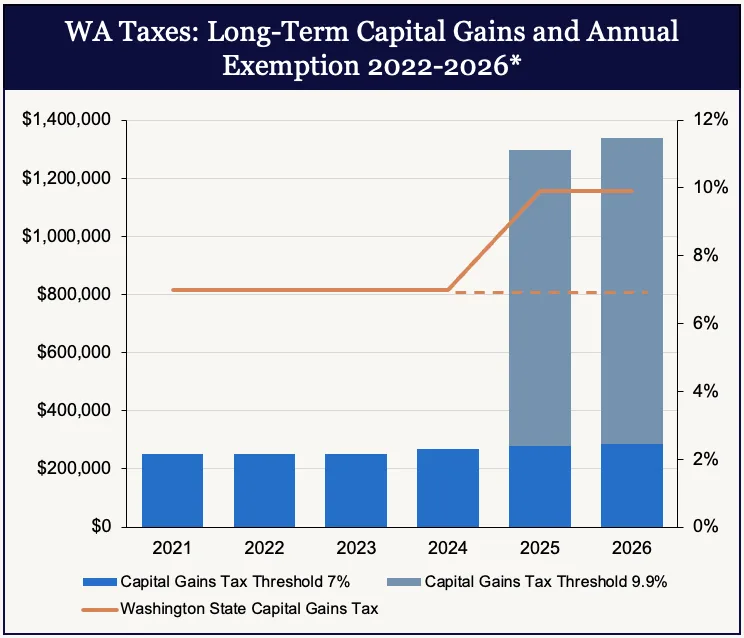

In July 2025, Washington rolled out significant updates to both its long-term capital gains tax and its estate tax framework. Beginning in 2025, the first $1 million of taxable Washington capital gains exceeding a $278,000 standard deduction (for 2025 and adjusted for inflation) is subject to a 7% tax, while gains above $1 million are taxed at 9.9%.

*2026 exemption not yet confirmed.

Source: taxfoundation.org; dor.wa.gov. Data pulled 1/2026.

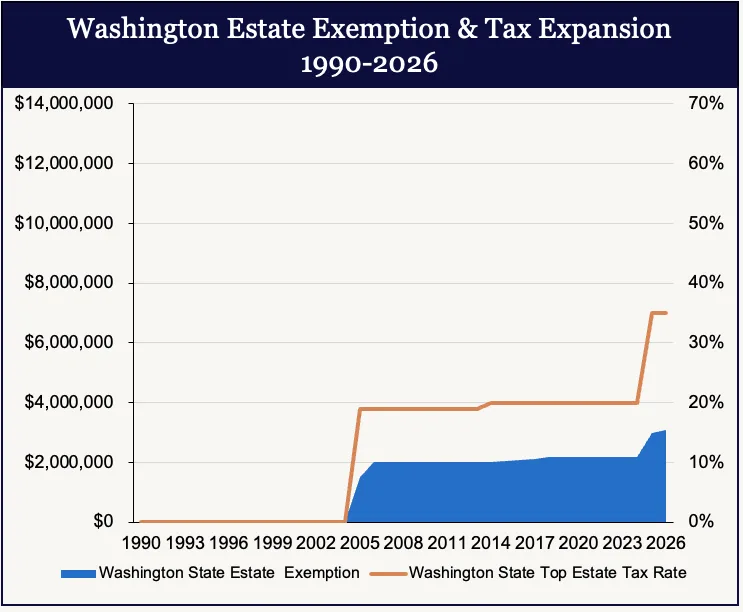

The estate tax exclusion increased to $3,000,000 for the second half of 2025 and is adjusted annually for inflation. Washington’s estate tax rates range from 10% to 35%, with the top 35% marginal rate applying to taxable estates above $9 million. As of March 11, 2026, lawmakers voted to roll back last year’s increase. If signed by Governor Ferguson, the top marginal rate would return to 20%, its previous level prior to the 2025 changes.

Source: michaelsonlaw.com; kiplinger.com; dor.gov. Data pulled 1/2026

When viewed together — a tiered capital gains tax, a revised estate tax framework, and a proposed 9.9% income tax on earnings above $1 million — Washington’s state-level tax structure for high-income households has evolved meaningfully in a relatively short period of time.

For a deeper review of the 2025 capital gains and estate tax changes, see our blog: Washington State’s New Tax Law: What It Means for You

Planning Considerations for High-Income Households

With capital gains tier changes already in effect and the income tax proposed for 2028, planning now spans across multiple tax years.

Several areas may be worth consideration:

Charitable Planning

Charitable strategies may play a larger role under a 9.9% state income tax rate. For Washington’s proposed Millionaires Tax, taxpayers may deduct qualified charitable contributions up to $100,000 per household if donated to a Washington-based public charity.

Consider:

- Bundling charitable deductions to maximize the $100,000 charitable deduction

- Opening or contributing to a Washington-based donor-advised fund (DAF)

- Coordinating larger charitable gifts with high-income years

Aligning philanthropic intent with tax efficiency can enhance both outcomes.

Deferring Income

Managing the timing of income recognition may become increasingly important.

Strategies may include:

- Considering installment sale structures for business or real estate transactions

- Maximizing deferred compensation arrangements

- Increasing traditional 401(k) and IRA contributions where appropriate

- Evaluating whether financing large purchases may help avoid triggering significant income recognition in a single year

The goal is to avoid unnecessary concentration of income in peak tax years when possible.

Timing Considerations

For individuals anticipating significant liquidity events, timing can be critical.

Planning may include:

- Evaluating whether certain liquidity events should occur prior to 2028

- Modeling income recognition across multiple years

- Reviewing residency planning before income is expected to exceed $1 million

Each strategy requires coordination with tax and legal advisors, particularly given evolving state-level rules.

Frequently Asked Questions About Washington’s Millionaires Tax

When would the Washington Millionaires Tax take effect?

If enacted, the 9.9% income tax on earnings above $1 million would apply beginning in tax year 2028, with returns filed in 2029.

Is the $1 million threshold based on salary only?

No. The threshold is based on adjusted gross income (AGI), which includes wages, business income, capital gains, bonuses, rental income, and other taxable income.

Will I be double taxed on capital gains?

No. Taxpayers are expected to receive a credit for any Washington capital gains tax paid, which would be applied directly against any Washington State Millionaire’s Tax owed.

Does the 9.9% tax apply to all income?

No. The proposed tax would apply only to income exceeding $1 million. For example, if a taxpayer earns $1.5 million, the tax would apply to $500,000.

How does the Millionaires Tax differ from Washington’s capital gains tax?

The Millionaires Tax would apply to income above $1 million. Washington’s capital gains tax applies to certain long-term capital gains. Beginning in tax year 2025, the first $1 million of taxable Washington capital gains is taxed at 7%, and gains above $1 million are taxed at 9.9%.

What is Washington’s estate tax exemption?

For deaths occurring July 1, 2025 through December 31, 2025, the exclusion amount is $3,000,000 and is adjusted annually for inflation. In 2026, the exclusion is $3,076,000. Estates above that threshold may owe Washington estate tax.

Can an estate owe Washington estate tax but no federal estate tax?

Yes. Washington’s estate tax exemption is significantly lower than the federal exemption. As a result, some estates may owe state tax even if no federal estate tax is due.

Who is most likely to be affected by these tax changes?

Business owners, executives, professionals with variable income, and individuals anticipating large liquidity events may be most directly impacted. Even one-time income spikes can create exposure in a given tax year.

With capital gains tier changes already in effect and the income tax proposed for 2028, planning now spans multiple tax years.

High-income households may want to review:

- Timing of liquidity events

- Capital gains realization strategies

- Income recognition planning

- Multiyear tax modeling

- State residency considerations

Why Proactive Planning Matters

Washington’s tax framework for high-income families has shifted in recent years. Capital gains now have tiered rates. Estate tax thresholds were increased but remain well below federal levels. A 9.9% income tax on earnings above $1 million may follow in 2028.

For families with complex income streams or significant assets, thoughtful, coordinated planning across income, capital gains, estate, and charitable strategies is increasingly important. If you would like to evaluate how these developments may affect your financial plan, we welcome the opportunity to connect. A Freestone advisor can help you model potential outcomes and integrate state tax considerations into a comprehensive wealth strategy.

Important Disclosures: This article is not intended to provide, and you should not rely upon it for accounting, legal, tax or investment advice or recommendations. We are not making any specific recommendations regarding any financial planning, investment or tax strategy, and you should not make any financial planning, investment or tax decisions based on the information in this article. This article is intended to be educational in nature and to discuss a few limited aspects of very complex legislation or other complex subject matters. This article is not a comprehensive or complete summary of considerations regarding its subject matter. We recognize that every individual has different needs and the opinions expressed in this article may not be appropriate for everyone. Please consult with a Freestone client advisor, accountant, or lawyer regarding options specific to your needs. Please note that Freestone does not approve or endorse any third-party content hyperlinked to in this article.